Unlocking the Next Retail Revolution: Returning to Experience and Efficiency

2023-11-06

How can investment identify and follow future trends while also following the laws of development? At present, China is moving from a large industrial country to a manufacturing power. The term Made in China now encompasses a wide array of industries, many of which are either born or innovated within the country.

In our Empowering Chinese Manufacturing series, we aim to distill the investment experiences of JD Capital across various sectors, elucidate the developmental trends within these industries, and continue offering equity investment services to the next generation of Chinese enterprises.

In this issue, we focus on the retail sector.

Shared by

Wang Chen, Managing Director, Consumer Investment Department, JD Capital

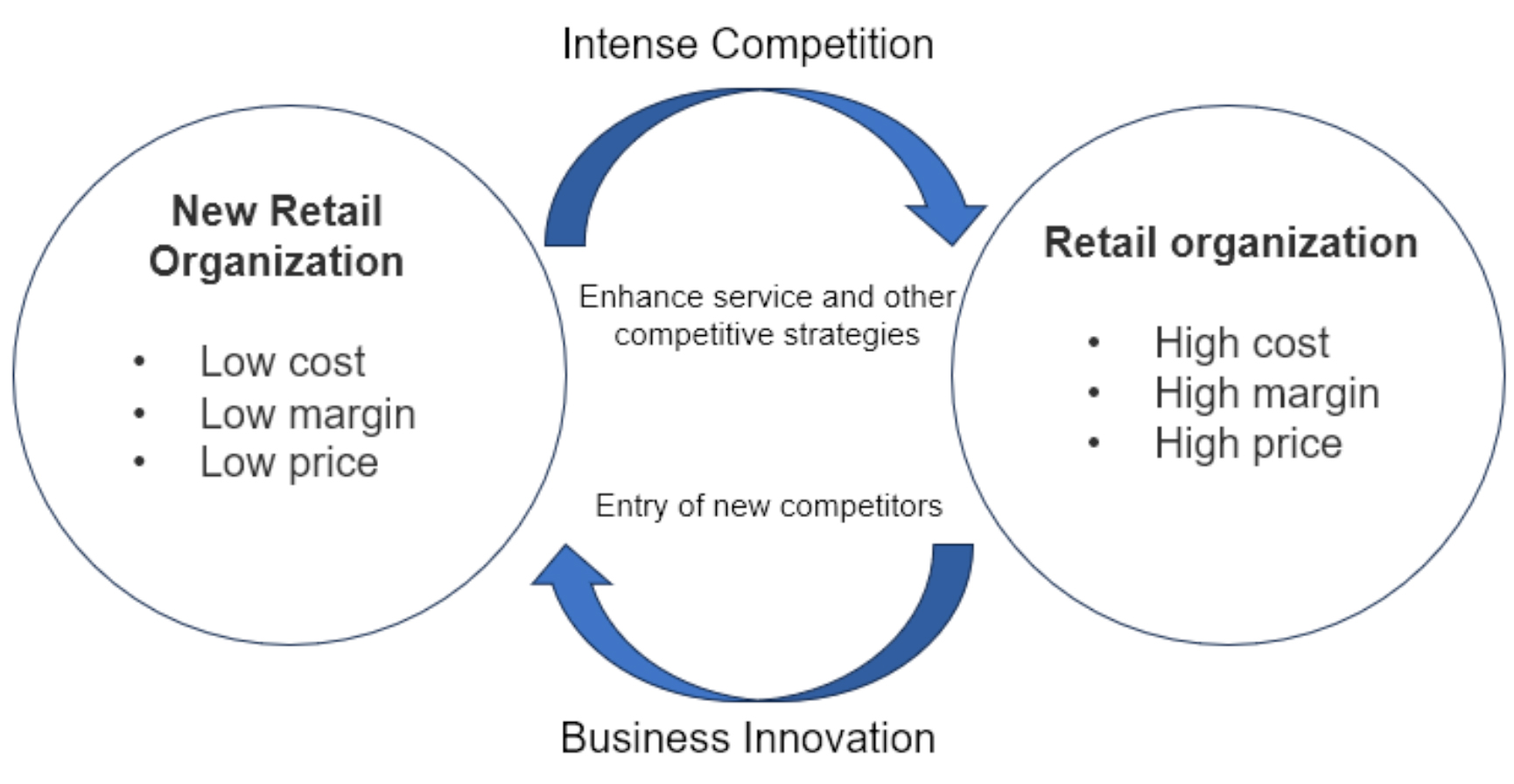

This summer, a price battle was ignited by durian mille-feuille. In early August, a customer reported that the price of a durian mille-feuille in Hema X had suddenly plummeted to RMB 99, prompting Sam's Club to retaliate with price reductions. Subsequently, Hema Fresh offered other popular items like Swiss rolls and mochi bread at lower prices to directly compete with Sam's Club. Concurrently, Meituan Grocery also launched special promotions and prominently featured a "Tug-of-War Price" label on its promotional page. This intense price competition has pitted the three retail platforms against each other. Behind this battle lies competition among warehouse membership stores and a broader rivalry among various retail formats.

Notes: Retail formats refer to various business models formed by retail operators by combining relevant elements to meet different consumer demands. Based on operational methods, product structures, service functions, and other factors, these formats can be categorized into 17 different types (according to the 2021 Chinese national standard), including convenience stores, supermarkets, shopping centers, specialty stores, and online retail.

Professor Malcolm P. McNair from Harvard business School proposed The Wheel of Retailing Theory in 1958, suggesting that retail organization transformation is cyclical, with a development trend akin to a revolving wheel. New retail organizations often enter the market with low profit margins, low costs, and low prices. When they succeed, it inevitably triggers imitation and competition. Intense competition then forces them to adopt competition strategies beyond pricing, such as improving services. As a result, increased expenses make them transfer into high-cost, high-profit, and high-price retail organizations. Meanwhile, new innovators with lower costs and lower profit margins enter the market, and the wheel starts turning again.

Looking back at the past thirty years of retail in China, mainstream formats have undergone changes. Whether it's the current popular warehouse membership/discount stores, or the previous shifts from supermarkets, shopping malls, e-commerce, convenience stores to online retail. Different forms of retail transformation have followed this trend. Since 2010, JD Capital has invested in shopping centers, convenience supermarkets, and retail stores in the South China. This includes investments in a shopping center operator WongTee International (000056.SZ), a convenience store leader Red Flag Chain (002697.SZ), home furnishing chain Easyhome (000785.SZ) and Fusen-Noble (002818.SZ), a braise snack brand Juewei Food (603517.SH), and a fruit chain Xianfeng Fruit, etc.

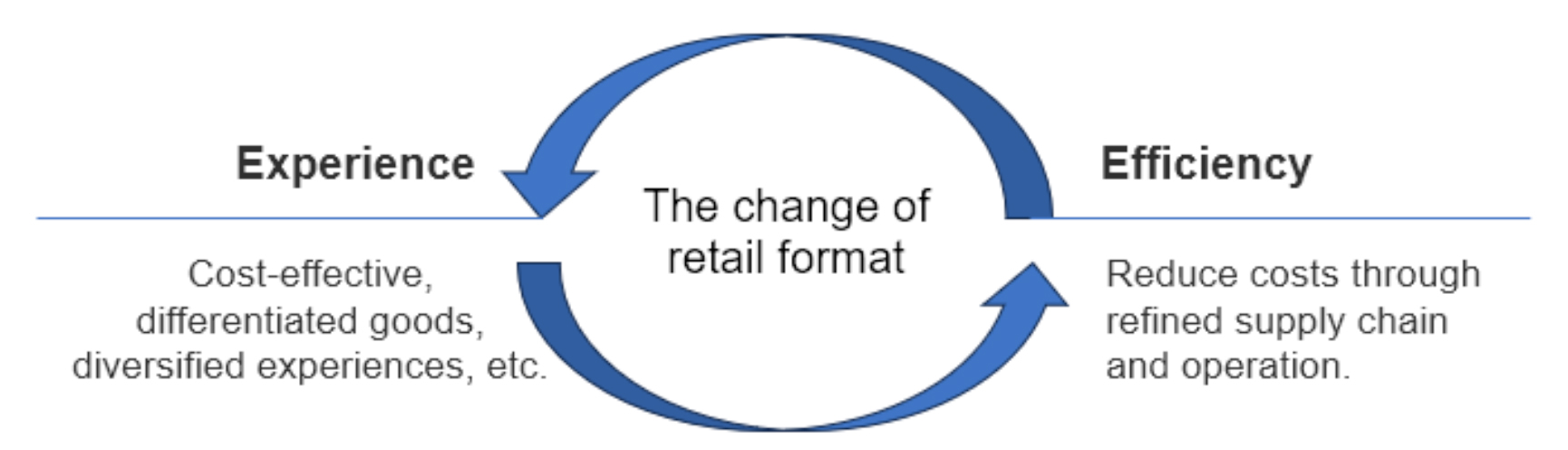

We find that behind the changes in retail formats are improvements in experience and efficiency. New retail organizations continuously satisfy consumer demands/experiences better through cost-effective, differentiated products while minimizing costs through refined supply chains and operations.

Today, the Chinese consumer market is entering a Resilience Era, with growth becoming increasingly rational. We have attempted to review more than a decade of investment experiences in the process of retail format changes and distill the underlying essence behind the transformation of formats. In the current phase of rotation in the consumption cycle and systematic cooling of consumption investments, JD Capital still believes that China's consumer foundation is highly resilient, and opportunities continue to exist in the upgrading of categories and channels, and industry cooling leaves room for investments.

Key Insights

1) The essence of retail is cost-sensitive, gross-profit-sensitive, and price-performance-sensitive. The core is to provide a better consumer experience (cost-effective products) with lower costs and higher operational efficiency.

2) In the new cycle, consumption is becoming more rational, but the trend of consumption upgrading still exists. Consumption upgrading is not at odds with a focus on price-performance. Retail formats that focus more on product quality, functionality, price-performance, and competitive pricing are more likely to stand out.

3) Any level of retail competition innovation can become the starting point for new formats, but only those that push the technological boundaries forward and successfully innovate can grow into mainstream formats.

1、Mainstream Retail Formats: Rising and Falling Over Thirty Years

➢ Experience Enhancement from Department Stores to Shopping Malls

In the 1980s, under the influence of China's reform and opening-up policies, a series of reforms, including separating government from enterprises and simplifying government functions, were implemented, and as a result, many large department stores with different ownership and operating models emerged.

According to data from the China Commercial Association, the number of large department stores with an operating area of 10,000 square meters or more on the Chinese mainland had increased from 10 in 1979 to 40 in 1994.

Department stores satisfied people's shopping needs with a wide range of goods. However, as material wealth gradually increased, people had higher expectations for the shopping experience, leading to the emergence of modern shopping malls that incorporated more dining and leisure elements. In 1996, the first large shopping mall in China, Guangzhou Tianhe City, was born, marking the beginning of the era of shopping malls in China.

After 2000, with the rapid development of China's economy and urban construction, the retail and real estate industries made significant strides, and the number of shopping malls grew rapidly, reaching nearly 4,000 by 2015.

During this period, JD Capital conducted intensive due diligence into over 600 shopping malls in 28 cities in China. The core threshold for shopping malls lay in massive capital investment and experience in commercial real estate operations. In the process of operation, competitive factors included location, market positioning, combination and supporting facilities, design, tenant recruitment, and operational management.

Taking JD Capital's investment in WongTee International in 2015 as an example, its core business was commercial operation services. At that time, the Shenzhen WongTee Plaza, operated by the company, was in the central business district of Shenzhen, with an excellent geographical location. Through differentiated management, tenant recruitment, and operational capabilities, WongTee International maintained a daily average customer flow of approximately 45,000 people from the end of 2013 to the end of 2015.

[Our observation]

During this period, the previous department stores were upgraded to shopping mall. The process of upgrading also showed us that during the leap-forward development of the market economy, the core of retail enterprises lies in establishing differentiation barriers around the consumer experience to meet ever-upgrading consumer demands.

➢ Downsizing and Localization in Supermarkets and Convenience Stores:

While shopping malls were rapidly developing, supermarkets also saw a period of rapid expansion. Policies played a crucial role in the initial development of the industry.

After 2000, with the agricultural reform (converting agricultural markets into supermarkets), a wave of construction of fresh food supermarkets swept across the country. From December 2004, China fully removed restrictions on foreign investment in domestic retail enterprises. Large foreign supermarket enterprises such as Walmart and Carrefour leveraged their advantages in global procurement, information technology, logistics technology, and advanced management technology to enter the Chinese market in the form of large supermarkets.

Therefore, domestic chain supermarket enterprises had to either work hard to improve their competitiveness, particularly in the fresh supply chain, as seen with Yonghui Supermarket, or focus on regional development to seek differentiated growth, as observed with Red Flag Chain, the largest convenience supermarket enterprise in southwest China.

In the 1990s, Red Flag Mall found itself in a dilemma in the state-owned retail industry. Cao Shiru, the manager of the Red Flag Mall Wholesale Branch at the time, discovered that there were almost no chain retail enterprises in Chengdu, but people had a demand for shopping nearby. Therefore, Cao Shiru came up with the idea of opening supermarkets based on the national supplier and warehousing network of the Red Flag Mall. In 1996, the wholesale company managed by Cao Shiru opened the first community supermarket in Chengdu. In 2000, Red Flag Chain was officially restructured and operated independently. In 2005, Red Flag Chain acquired Red Flag Mall. Subsequently, Red Flag Chain entered a period of steady development, and JD Capital began to get in touch with Red Flag Chain.

According to the experience of developed countries, large comprehensive supermarkets begin to rise when per capita GDP exceeds US$3,000, and after per capita GDP exceeds US$5,000, the convenience stores begin to grow. Beyond US$10,000 per capita GDP, convenience stores are expected to enter an explosive growth phase. In 2010, Sichuan Province, covered by Red Flag Chain, had a per capita GDP exceeding US$3,000, and the per capita GDP of Chengdu was close to US$6,000, which was the period of rapid development for convenience supermarkets. Moreover, at the time, second and third-tier cities, with relatively higher purchasing potential and lower operating costs compared to first-tier cities, were gradually becoming the focus of large retail chain enterprises.

Facing foreign supermarkets, Red Flag Chain adopted a different competitive strategy, defining it as convenience supermarkets, positioned between supermarkets and convenience stores. The format primarily targeted residential, school, business, and entertainment districts and operated as a convenient supermarket retail format with the characteristics of convenience and trust. It sold food, tobacco and alcohol, daily necessities, and provided services such as public transportation card top-ups, telecom bill payments, and electricity bill top-ups. It had the network effect of convenience stores and a rich category supply of supermarket formats.

At the same time, Red Flag Chain focused on regional development. The barrier to entry into the convenience supermarket industry was not high, and the profit margin was relatively low. The challenge lay in improving fine management and high efficiency to achieve economies of scale and establish a brand. Red Flag Chain already had the foundation in Sichuan, including brands, store networks, and procurement channels.

At the time, upstream suppliers generally operated under a regional agency system, with multi-layer distribution systems mainly based on provinces or cities. Focusing on regional development can also improve bargaining power. However, it also made it challenging to expand across regions.

[Our observation]

Comparing comprehensive supermarkets represented by Yonghui and regional convenience supermarkets represented by Red Flag Chain, we can see that, relative to traditional farmers' markets and mom-and-pop stores, supermarkets have excelled by continuously refining their supply chain and operational management, offering a one-stop shopping experience for both standardized and specialized products. Their neatly organized displays, standardized pricing, and services cater to the trends of consumer upgrading.

In recent years, traditional large supermarkets have gradually declined, while convenience stores have experienced gradual growth. We believe that the core is that convenience stores focus on consumer needs, optimize supply chain and logistics efficiency, which offers a faster and better shopping experience. In 2019, China's per capita GDP exceeded US$10,000, providing support for the single-store model of convenience stores.

➢ Retail Specialty Stores: Categories and Replicability

Retail specialty stores primarily sell a specific category of products, reflecting specialization, depth, a wide variety, and sometimes offer expert advice. During China's urbanization process, the increasing urban population led to the rise of retail specialty stores that catered to various specialized and local shopping needs, such as Juewei Food, which specializes in duck products and braised snacks.

The founder of Juewei, Dai Wenjun, made a mid-career decision. In 2005, at the age of 37, he resigned and started his own business. At the time, brands like Zhou Hei Ya were already well-known in the leisure braised food market, but the market was still quite fragmented. Dai Wenjun believed that there was an opportunity to create a national chain brand in this segment. As residents' income levels rose, coupled with the modernization of the food industry and mature infrastructure like logistics, snack foods became one of the fastest-growing segments in the food industry. Therefore, Juewei decided to shift its focus from a staple to a snack food. In April 2005, Juewei's first store opened. Several years later, JD Capital began to engage with Juewei.

During the due diligence process, we found that:

1) In terms of retail terminals, Juewei invested significantly in franchise stores compared to other braised snack brands at the time. In the franchise model, Juewei produced the braised snacks and delivered them to various franchise stores daily. To reduce the entry barriers for franchises and enhance control, Juewei introduced a series of standardized and supervisory measures, which makes it does not face issues like inventory pressure or high selling expenses. Juewei could swiftly recoup capital and accelerate inventory turnover. This franchise model laid the foundation for Juewei's rapid expansion within a few years.

2) The duck braised snack industry had already undergone industrialization for a decade, and competition was intense. The industry had shifted into a brand competition era, and Juewei had advantages in terms of brand and scale.

3) In the supply chain, the above-mentioned advantages also gave Juewei strong bargaining power over upstream raw material suppliers and downstream direct customers. This allowed them to have a certain profit margin. Juewei addressed cleanliness, hygiene, and taste standards in the braised snack industry, established barriers in the production process, and generated premium value.

Rising income levels not only fueled growth in the snack food market but also stimulated fruit consumption. The market for fruits, which represent natural and healthy choices, displayed an upgrading trend. During the same period, another type of retail specialty store emerged, represented by Xianfeng Fruit, specializing in fresh fruits.

In 2004, the year before Juewei's first store opened, Han Shuren opened the first Xianfeng Fruit store in Hangzhou. Han Shuren, originally from Anhui, moved to Hangzhou to start his life when he was 18. During his early years in Hangzhou, he pushed a tricycle and sold fruit on the sidewalk. One day, he was inspired by the story of Sam Walton in the book The Walmart Way. Then je decided to start his own fruit supermarket.

By 2010, Xianfeng Fruit's number of stores had reached 50, marking the expansion beyond Hangzhou. During this time, JD Capital found that China was a major consumer of fruit and got in touch with Xianfeng Fruit. At that time, the fruit retail industry had low concentration and was relatively decentralized both upstream and downstream. The primary retail outlets for fruits were mom-and-pop stores, but they had high procurement costs due to their small scale. Supermarkets lacked advantages in terms of store opening speed and convenience. E-commerce had issues with high losses and difficulties in fulfillment. In contrast, fruit chain stores were more agile and community-oriented in their management. With the growth in the number of stores, there was further room for reducing procurement and distribution costs.

As a result, JD Capital predicted that the growth rate in this specialized area of fruit chain supermarkets would exceed overall fruit consumption for some time. Furthermore, Xianfeng Fruit had the following characteristics:

1) In terms of products and the supply chain, Xianfeng Fruit used a direct procurement model from farms to ensure the long-term reliability and quality of upstream products. It established long-term cooperative relationships with planting bases in China, and gradually increased the proportion of directly imported fresh fruits to meet the demands of upgraded fruit consumption. Moreover, by shortening the supply chain and enforcing strict standardization and process execution in quality control, Xianfeng Fruit ensured freshness management and loss control management.

2) In terms of store operations and expansion, leveraging long-term accumulated experience and related data, they analyzed and designed shelf and counter display guidelines to enhance store space utilization efficiency. They followed the principle of using high-frequency & low-margin consumption to drive low-frequency & high-margin consumption, achieving an overall balance of profits. Additionally, they used data analysis through information systems to adjust the inventory and the sales of each store. Furthermore, to improve the replicability of their stores, Xianfeng Fruit summarized six factors, including market capacity, district atmosphere, convenience, store attributes, competitive environment, and store rent, to standardize the site selection process.

Apart from the retail specialty stores in areas such as snacks and fruits, this period coincided with the rapid urbanization in China, which drove the prosperity of the building materials and home furnishings market. Taking our investments in EasyHome and Fusen-Noble as examples, during the era when real estate served as the backbone of the national economy, these retail formats specializing in home decoration and building materials experienced rapid development.

[Our Observation]

The development of different types of retail specialty stores in various domains varied significantly, but they also displayed common characteristics. We find that retail specialty stores meeting these characteristics are more likely to show growth:

1) Categories that are broad, have a large market size, and are trending upward in demand tend to be more valuable. Categories that cater to niche markets might experience temporary success but could be short-lived.

2) Compared to general retailers, specialty stores catering to specific product categories can enhance customer experiences and operational efficiency. They can better meet specialized customer needs, such as optometric services in eyeglass stores or delivery and installation services in home appliance retailers.

3) Specialty stores with a high degree of product standardization and relatively low supply chain complexity, including raw material sourcing and logistics, are more likely to expand rapidly.

➢ Beware of Cost Traps in Online Retail

In 2014, the proportion of e-commerce in China's social retail product consumption market exceeded 10% for the first time. 4G technology became widespread, and the rise of smartphones sparked a new era of affordable smartphones. The wave of mobile internet reached down to the lower-tier markets. This transformation was accompanied by the decline of large supermarkets, as well as the rise of more convenient convenience stores and online shops. Department stores specializing in clothing and footwear, and electronics markets centered around digital home appliances, were particularly hard-hit by the impact of e-commerce. This period marked a turning point for the retail industry in China. Subsequently, new online formats and models related to e-commerce continued to emerge, including various O2O models, fresh e-commerce, new retail, community group buying, social commerce, and live streaming e-commerce.

Online retail broke free from the constraints of time and space, offering limitless supply and introducing a rating system. The gradual improvement of logistics networks laid the foundation for the diversification of online formats. However, in recent years, the costs of acquiring traffic and fulfilling online orders have steadily increased. Online retail, often in a land-grab phase, selectively overlooked costs and efficiency. For instance, some fresh e-commerce companies adopted high-cost approaches that proved unsustainable. Eventually, in the face of intense competition, exceptionally high operating costs inevitably weighed down these companies.

[Our Observation]

After enduring fierce competition, whether online or offline, we believe that the essence of the retail industry is cost-sensitive, margin-sensitive, and value-for-money-sensitive. Its core lies in providing a better consumer experience with lower costs and higher operational efficiency. Regardless of how the economic cycle revolves, every wave of retail disruption has seen newcomers originating from the fringe markets, replacing or disrupting existing formats with this model.

2、what types of retail are more likely to thrive in the age of resilience?

Today, with large supermarket on the decline, convenience stores maintaining steady growth but not expanding rapidly, and specialty stores experiencing both openings and closures.

So what types of retail are poised for success in the future? We believe that the Chinese consumer market is entering an era of resilience characterized by rational growth. China's per capita GDP has remained above US$12,000 for two consecutive years, with per capita disposable income increasing year by year. According to data from McKinsey Global Institute, from 2019 to 2021, the CAGR of Chinese urban households with annual incomes exceeding RMB 160,000 (approximately US$21,800) reached 18%, growing from 99 million to 138 million. By 2025, an additional 71 million households are expected to enter this higher income bracket. Besides, since the onset of the Covid-19, there has been a phase of reduced consumer confidence, with a 0.2% decline in total retail sales of consumer goods in 2022 compared to the previous year.

Under this situation, JD Capitals believes that consumers will become more rational. This translates to a renewed focus on product quality and functionality, signaling a return to the principle that product is king. In terms of channels, consumers will prioritize value for money, favoring channels that offer competitive prices. In the long term, the trend of consumer upgrading is expected to persist, creating new opportunities. However, with different consumer segments experiencing both upgrading and downgrading of consumption, consumer upgrading and a focus on value for money are not mutually exclusive.

As China's per capita GDP increases, Chinese retail formats are expected to follow global trends, moving towards smaller, community-based formats. However, they also have unique characteristics as follow:

1) China's online retail formats are leading the world, with innovations and differentiation that set the global standard.

2) China has mature supply chains, resulting in relative oversupply in certain categories like apparel and home goods. In both domestic and global markets, there's substantial room for discount based on these categories.

3) More importantly, China's market is vast and has distinct consumer segments. Different retail formats exhibit varying growth trends in different regions. For example, in-depth visits to Chinese county-level cities revealed that large supermarkets have become more popular in these areas in the past two years. This is because large supermarkets fail to meet the fast requirement, which is less significant for consumers in county-level cities compared to the demands for good and affordable products.

Japanese retail expert Masanori Nakata points out that the Wheel of Retailing theory does not explain the innovation of retail companies across different price levels. He emphasizes that new-format companies do not drive out old-format companies due to their cost structures. Instead, they gain a competitive edge by moving the technological boundary. The lowest retail price required to achieve a certain service level is called the technological boundary. Low price and low service are by no means the characteristics of new-format companies. Retail innovation can start at any price level, but only those that push the technological boundary forward and succeed in innovation can become mainstream.

In recent years, membership stores and discount stores that have demonstrated resilience aim to push the technological boundary forward.

➢ Typical Format I: Warehouse Membership Stores

In the 1990s, foreign retail giants introduced the membership model to China. However, due to various factors, this model did not experience rapid growth initially. In recent years, the market size of warehouse membership stores has continued to grow, and after local innovations, it has expanded rapidly. Based on the experiences of developed countries, the membership model usually emerges when the per capita GDP reaches US$10,000, targeting the middle class with homes, cars, children, and busy jobs. China reached this per capita GDP milestone in 2019, with over 200 million private cars in circulation, ushering in the era of membership stores. Companies like Sam's Club and Costco have demonstrated a positive business model built around consumer demand + single-store model + supply chain logistics. Warehouse membership stores select a limited SKU range, expand the scale of single-item procurement, optimize supply chain logistics, and offer consumers high-quality products at low prices.

Product selection and supply chain optimization are two significant competitive advantages of these international giants. For local enterprises, improving product selection and research and development, as well as enhancing the strength of their private labels, is crucial. The former requires finding high-quality products from reliable suppliers, while the latter involves achieving product innovation and production through insight into consumer needs and collaboration with suppliers. Establishing private labels is one of the future trends in retail formats, belonging to the category of manufacturing-type retail.

One of the logics of retail is turning trust into revenue by building trust with consumers through store and brand image, and selling products under their private labels. He Houyi, CEO of Hema Fresh, concluded after visiting leading retail giants worldwide that nearly all advanced retail businesses globally rely heavily on their private labels, accounting for roughly 60-70% of their product offerings. These retail companies focus on two critical aspects. Firstly, under globalized procurement, they leverage resource integration to find cost advantages. Secondly, they build a commodity differentiation capability based on consumer demand, enhancing profit margins while escaping the mire of homogenous competition.

However, the upgrading of products and supply chains requires the gradual maturity and development of the entire ecosystem, rather than relying solely on innovations within specific retail formats. Therefore, JD Capitals believes that warehouse membership stores in China will maintain stable growth, but their expansion rate will not be too rapid. Ultimately, all forms of retail organizations must return to industry realities and be willing to take the long road, opting for a steady pace over haste.

➢ Typical Format II: Discount Stores

In the age of resilient consumption, the pursuit of value for money is a defining characteristic, particularly during economic downturns when consumers actively seek discounts and promotions. Globally, when economies shift into a phase of moderate to low growth, both online and offline low-price discount retail formats tend to thrive for an extended period. Classic examples include a China e-shopping firm PDD and Dollar General, a U.S. discount retail chain.

In comparison to comprehensive discount stores, JD Capitals has found that snack discount stores have experienced exceptional growth over the past few years. According to incomplete data from CITIC Securities, by the end of 2022, there were already over 10,000 snack discount stores in China. Furthermore, research estimates from Huachuang Securities anticipate that the number of domestic snack discount stores could reach 30,000 by 2025. The primary reason for this is that snack consumption satisfies immediate needs, and local community stores play a valuable role in this regard. Additionally, the richness of snack products and their affordability generally align with the "multi, quick, good, and affordable" consumer demands.

In terms of single-store costs, discount stores essentially aim to reduce procurement prices by optimizing the supply chain. The headquarters of snack discount stores directly negotiate cash purchases with brand manufacturers, eliminating the need for fees related to entry into supermarket systems, barcodes, and promotional displays, in exchange for preferential purchasing prices. Furthermore, this eliminates the lengthy distribution chain involving multiple intermediaries.

In comparison to other categories, snacks have a distinct advantage when it comes to terminal procurement pricing due to the interplay between brands and channels. Because the snack category faces oversupply, the influence of channels is relatively stronger compared to certain brands. Consequently, snack discount stores possess significant bargaining power. Furthermore, models such as setting up stores in underserved communities and optimizing warehousing through consolidation have enhanced the single-store model.

According to calculations by JD Capital, snack discount stores can achieve a cumulative price increase from production to the final storefront much lower than traditional distribution channels, making their prices 20% to 30% cheaper than supermarkets/high-end snack stores and 30% to 50% cheaper than other channels, thus offering a competitive alternative.

In terms of supply chain and logistics, snacks do not require refrigeration, have longer shelf lives, and have relatively lower warehousing, logistics, and fulfillment challenges. So, what are the characteristics that can help snack discount stores succeed in this current land-grab phase? We believe that the following five aspects should be considered:

1) Timing. Snack discount stores are a type of business format where the advantages of being an early entrant are quite evident. This is because the industry is highly competitive and homogeneous, with relatively manageable supply chain complexities, allowing for rapid expansion. The industry is growing fast, and missing the right timing can make it difficult for latecomers to catch up through differentiation. Specialty stores can differentiate through category innovation. Convenience store industry trends are positive but slower. Supermarkets face greater supply chain complexities in their early stages of development, and easy expansion across regions can lead to losses. Hence, early entry advantages are not as pronounced in these cases.

2) Product. This includes product selection and iteration. Finding the right product mix, updating products in a timely manner, and coordinating with the supply chain for adjustments are core capabilities for snack discount stores.

3) Scale. Having a better single-store model that can attract more franchisees and achieve rapid store expansion replication gives companies a better chance of success.

4) Supply Chain. Like other retail formats, success depends on the ability to select and maintain suppliers as well as control warehousing and logistics.

5) Strategy. This is manifested as a competitive advantage within a specific region. For example, snack discount stores headquartered in the western regions may find it easier to radiate throughout the entire Southwest and Northwest regions, establishing a competitive edge within their specific area compared to competing in regions with a larger number of snack discount store brands in the East.