JD investment Insights:Key investment opportunities in the power battery supply chain, reflecting on ten years of power battery development.

2023-06-15

Abstract: Survival hinges on technology, while longevity is contingent upon cost effectiveness.

[Opening Note]:

Over the past four decades, China has rapidly risen in many fields, proving the longevity of “Made in China”: massive market scale, mature industrial chain support, and endogenous solid dynamics of market participants creating a world-renowned economic growth rate and industrial results.

Today, China is moving from a “Major Manufacturing Country” to a “Manufacturing Power.” The new generation of “Made in China” is no longer about good quality with low prices, nor is it simply about domestic substitution, but about industrial upgrading through independent innovation and participation in global competition.

As a PE firm focusing on equity investment for more than ten years, JD Capital has served many outstanding “Made in China” companies in various fields along the line of the rise of “Made in China.”

Standing at the starting point of the new cycle, we try to review our past investment experience in major industries, sort out the laws of industrial development, and continue to serve the new generation of “Made in China” with equity investment.

In the first issue, we focus on the power battery industry chain.

On the one hand, is the violent shock of raw material prices. On the other hand, is a new generation of batteries installed in the imminent market expectations. In 2023, the power battery industry came to the crossroads of development again.

JD Capital has been focusing on the power batteries industry represented by lithium battery since around 2010. In the last decade of the industry development, it has invested in several companies along the upstream of the industry chain, one after another.

Reviewing the development of China’s power battery industry chain over the past ten years, “policy support,” “cost reduction and efficiency,” and “domestic substitution” are the three key words: under policy support, achieving cost reduction and efficiency through technological breakthroughs and supply chain advantages, and finally complete the domestic substitution of the industry chain.

Standing at the junction to the next decade, JD Capital believes that: the traditional lithium battery industry chain has already seen a phase of overcapacity, and the industry is about to enter a reshuffle period. However, the power battery market is not settled, and new technologies will still reshape the industry upstream and downstream.

1.Industry development in the first decade:Policy boosts and domestic substitution sit on the table

The industrialization of lithium batteries began in Japan in the early 1990s. Sony began to produce 18650 lithium batteries. From that time, lithium batteries began the process of dramatic industrial change.

By 2010, small lithium battery technology was well established, and its applications expanded due to its apparent advantages. According to the Japanese consulting firm IIT’s sales statistics in 2010, from the point of view of the global use of lithium batteries at that time, 49% of the global lithium battery cells are used in mobile electronic devices such as cell phones, 36% in notebook computers, 5.5% for other consumer products, and only 0.2% for new energy vehicles.

However, there was already a partial market consensus at that time on the future application of lithium batteries in large batteries, namely, automotive power batteries and energy storage batteries.

The fact is also actual. Along with the new energy vehicle industry, more than a decade since then, the power lithium battery opened the industry leap.

Chinese companies’ efforts in the power battery industry chain began with the emergence of the downstream new energy vehicle market. What kicked off the development of new energy vehicles in China was the “Ten Cities, One Thousand Vehicles” pilot program in 2009.

At the 2008 Beijing Olympics, 50 pure electric buses travelled to and from the Olympic Center, achieving zero emissions in the Olympic Center for the first time in international Olympic history. Six months later, the Ministry of Science and Technology, Finance, the Development and Reform Commission and Information Technology jointly launched the “Ten Cities and Thousands of Energy-saving and New Energy Vehicles Demonstration and Application Project.” Since then, with the support of financial subsidies, the “new energy on board” campaign pressed the accelerator button.

But now, the upstream power battery market is still in the hands of the Japanese and Korean lithium giants. Tesla, which launched the first electric car Roadster in 2008, entered into a partnership with Panasonic, which enabled Panasonic to harvest an unprecedented number of sky-high orders and established its global power battery dominance for a while.

In China, only several small lithium battery enterprises developed by the east wind of consumer electronics. In the field of power batteries, Chinese enterprises not only seriously lack of competitiveness in technology, but also to face the siege of the Japanese and Korean giants.

In 2010, Japan released its “Next Generation Vehicle R&D Strategy,” choosing to bet on hydrogen fuel cells and voluntarily abandoning lithium batteries for power.

A landmark event followed: Zeng Yuqun left ATL’s parent company to set up Ningde Times and took advantage of the space to take orders from BMW, forming own production specifications with the help of power battery production standards provided by BMW. With the backing of BMW’s core suppliers, Ningde Times quickly got orders from many car giants.

What also turned the tide was a series of policies introduced in China.

Unlike Japan, China, as a significant automobile producing and consuming country, has always been lagging behind in the field of traditional automobile-manufacturing. Therefore, the government attaches great importance to the research and development of electric vehicles, hoping to use it to achieve leapfrog development. Around this goal, the government’s support for power lithium battery has also been placed within the general framework of electric vehicle industry development.

By 2015, China began to implement the power battery “white list system,” the enterprise only the “white list,” equipped with its powerful battery new energy vehicles can enjoy subsidies. Before and after the “white list” of four batches of enterprises were all local enterprises, Panasonic, Samsung SDI, LG Chemical and other Japanese and Korean giants were rejected.

n 2019, the “white list system” was abolished. According to a research report by East Asia Qianhai Securities, Chinese companies are the most numerous among the top 10 global power battery companies in that year. Ningde Time and BYD have been among the first echelon of power lithium, enough to compete with the Japanese and Korean Lithium giants.

More than a decade of policy escort industry to accelerate the promotion of China’s lithium industry to sit on the world’s card table.

2.Behind the rise of the industry:How to invest deep into the industry chain?

The continuous surge in downstream demand has also led to a rapid boost in raw materials and equipment in the upstream of the industry chain in the last decade.

Around 2010, Japanese and Korean lithium battery practitioners mastered the core technology and have more insight into the market channels, and are good at capturing the changing trends in the consumer and mobile electronics and other application product markets to deal with market risks.

But the power battery market is much broader and needs more support from policy, consumer demand, and industry chain foundation. In the future, in the game with China, Japan and South Korea do not have an advantage in these aspects.

Japan and South Korea’s large, traditional, proud of the fuel car industry, also limit its “wheel turn” speed, will and determination, resulting in the two countries failed to continue its position in the field of power batteries in the consumer electronics industry lithium hegemony.

Compared with South Korea and Japan, JD Capital believed that China’s advantages could be summarized into three aspects when examining the industry chain:

1,Low manufacturing costs. China has inexpensive and abundant labor resources, bargaining power for bulk raw materials, port shipping capacity and abundant inland waterway transportation capacity, resulting in a low-cost competitive strategy. It can be said that in addition to the scale of expansion, the world lithium-ion battery market in the previous two decades of rapid price declines, basically from Chinese companies to pull.

2,China has the world’s largest consumer market.

3,China has formed a relatively complete industrial chain of lithium-ion batteries, and has certain advantaged in the supporting of lithium-ion battery materials.

From the distribution, the manufacturers of lithium-ion batteries in China were mainly concentrated in Guangzhou, Tianjin, Shandong, Jiangsu, Zhejiang and other places. The production of lithium batteries in South China (Guangdong and Fujian) accounts for 65% of the domestic market share. The most representative of lithium production in South China is Shenzhen, which is home to many well-known enterprises such as BYD, forming an industrial cluster.

In terms of disadvantages, Chinese companies are clearly deficient in core technology development. In addition, Chinese companies are generally small in scale and lack international development experience.

At that time, the lithium battery belongs to the high-growth industry, but without a certain amount of capital, scale and technological strength of the company is also difficult to stand.

Therefore, JD Capital believes that in order for China’s lithium industry not to be constrained by others and to establish long-term competitiveness, it is necessary to improve the localization rate of each link through technological breakthroughs. The investment institutions should dig deeper into the key links of the industry chain, find the enterprises with competitive barriers, and support them to become large-scale and achieve domestic substitution.

How to find valuable links in the chain?

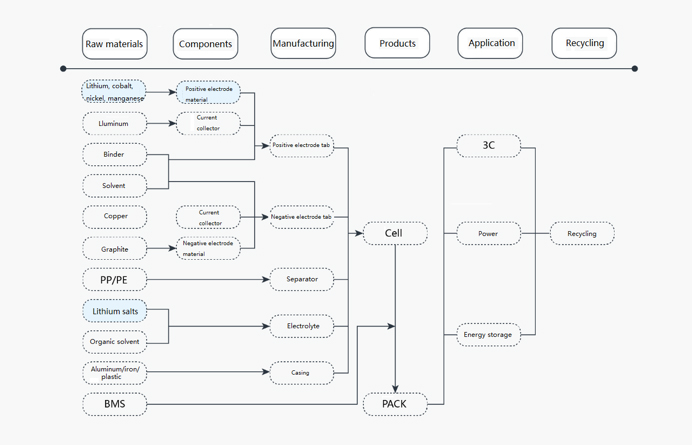

Lithium batteries are mainly composed of positive electrode, negative electrode, diaphragm, electrolyte and other auxiliary materials.

When the battery is charged, the lithium ions are detached from the positive electrode under the action of the applied power supply and move through the electrolyte and through the diaphragm to the negative electrode where the lithium ions can be embedded. When the battery is discharged, the lithium ions embedded in the negative electrode are separated from the negative electrode and flow to the positive electrode through the electrolyte, while the electrons move accordingly in the external circuit to form a current.

(Figure-Power lithium battery material industry chain)

Further research on power lithium battery, JD Capital found that because electric vehicles need high power electricity, in actual use, thousands of cells are often used in series and parallel to form modules and PACK to ensure the supply of energy. Therefore, the consumption of lithium battery materials for electric vehicles is equivalent to tens of thousands of times that of conventional batteries.

According to the estimation of JD Capital in 2010, the lithium-ion battery-related materials required for the production of only one million electric vehicles would be several times of the total global demand for lithium battery materials at that time, which implies a huge incremental opportunity behind.

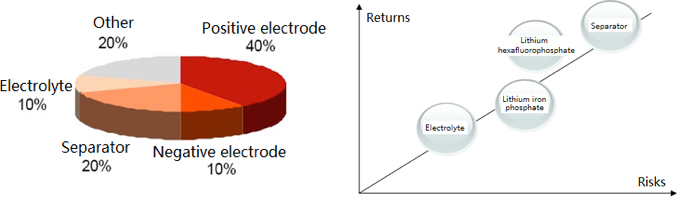

As can be seen in the figure, cathode materials account for the highest cost ratio, followed by diaphragm and cathode materials. And from the comparison of technical difficulty and revenue matching, the diaphragm has the highest technical content, but its corresponding revenue is also the highest.

(Figure-Power lithium battery cost composition & value analysis)

At that time, how to determine the competitive barriers of industry chain companies?

We have combed through a large number of domestic positive and negative electrode materials and diaphragm companies contacted/researched/invested bu JD Capital around 2010, and tried to find some elements from them:

1,Technical Strength

To diaphragm, for example, 2010 data show that the demand for diaphragm in China in 120 million square meters, but 80% need to rely on imports.

Because of the late start of domestic diaphragm research and development, performance and mass production stability is poor, mainly for the global low-end market. Although the prices is only 1/2 to 1/3 of imported products, but by the patent and technical process limitations, has never been able to compete with imported products.

JD Capital learned from the research that the gap of domestic products mainly lies in the performance indicators can not be taken into account as a whole, the stability of mass production batches is poor, not suitable for high-end products (including power battery separators) with high requirements for consistency and uniformity.

Therefore, whether the company can master the key production technology and whether the customers can accept the product is the key point. And JD Capital optimistically estimates that this process will take at least 2-3 years.

Therefore, at that time, a small number of Chinese companies that had independently mastered the key technology and obtained customer certification, there was a greater opportunity for domestic substitution.

Similarly, the first thing potential competitors will encounter when entering the negative electrode materials market is the technical barrier. In those days, many people could do the primary products of negative electrode materials, but small enterprises did not have the strength of continuous technological improvement and research and development. They are often mastering a product formula to crudely seek low profits, lacking long-term growth.

2,Alternatives (technology iteration)

Lithium batteries face numerous alternatives to other forms of electrochemical energy storage, such as fuel cells. Therefore, judging the substitutability of existing products and technology paths is crucial from the perspective of technology iteration.

For lithium battery, JD Capital’s judgment in 2010 was that it would be the mainstream in the predictable ten years as the rechargeable battery with the best application performance, more mature technology and more excellent prospect at that time. However, the manufacturing of batteries is continuously improving, and the downstream demand for positive and negative electrodes, diaphragm materials, electrolytes, battery packaging methods, etc., is constantly improving.

For example, in terms of negative electrode materials, the most widely used and matured at that time was the modified natural graphite in carbon materials. During the research, JD Capital learned that graphite is rich in resources and mature technology suitable for use as anode material, and the market pattern of dominance will not change quickly.

Other new materials that were more researched then and had achieved some application results were mainly different carbon materials. Still, their relationship with modified natural graphite was not a complete substitution. Lithium titanate, silicon-based anode and other new materials, the world is at the beginning of the research stage, from the development and application of a long time.

Therefore, companies with technology paths and products that are difficult to replace in the short term and can lay out in advance in terms of relevant technology reserves are more competitive.

3,Industry competitiveness

Taking cathode materials as an example, through research on downstream battery companies and competitors, JD Capital understands that the barriers of cathode materials companies are mainly reflected in the core parameters of the products and the effect after being made into batteries. For example, the core indicators for producing battery-grade iron phosphate are the molar ratio of iron to phosphorus, product nanosize, and proper crystal structure. The key lies in the production process, equipment and the ability to find the best know-how. For downstream battery companies, it is necessary to ensure the consistency and reliability of continuous production.

Similarly, internationally renowned lithium battery manufacturers will require a perfect quality control system before forming a stable partnership with lithium battery cathode material manufacturers, thus ensuring product stability and high consistency.

This requires material suppliers not only to master and apply advanced production site management methods, quality management tools and systems but also to have precise operational standards, testing standards and high-level professional production processes.

After passing the on-site quality system audit and comprehensive certification of material suppliers from raw material procurement, production management capability, product consistency, supply capability and after-sales service, it is still necessary to go through long-term friction of production process matching between the two sides to finally form a stable cooperative relationship.

Once lithium battery companies and materials form a close partnership, they will not easily change suppliers. Therefore, it is difficult to break through the lithium material producers who have passed the quality certification of large domestic and foreign customers at that time.

4,Upstream bargaining power

Most of the primary raw materials for lithium battery materials are bulk petrochemicals and non-ferrous minerals. We can have upstream solid bargaining power if we can enhance the procurement volume through the scale effect.

In addition, the focus of business operations is the ability to establish a relatively solid upstream and downstream cooperation relationship to avoid the squeeze of suppliers to enterprises in procuring raw materials.

5,Downstream bargaining power

The downstream customers for lithium battery upstream enterprises, are power lithium battery manufacturers, which are generally large in scale and have stronger bargaining power. Therefore, it is essential for companies to strengthen their downstream discourse by continuously enhancing their product power to occupy market’s mainstream.

Overall, the history of the rise of China’s lithium industry chain is also a history of “Made in China” catch-up. In addition to technical strength, production capacity and product stability, scale effect, cost and efficiency advantages is the key to the industry’s long-term competitiveness in the middle and late stages of development, which is also the underlying logic of the manufacturing industry in general.

3.The Road to the Next Decade:What’s more than Lithium?

Line to 2023, overcapacity has become the biggest worry of the power lithium battery industry.

Statistics from the China Power Battery Industry Innovation Alliance show that with 2025 as the node, only 6 head enterprises such as Ningde Time, BYD and China Innovation Airlines are planning to reach 3039GWH in production capacity. According to the analysis data published by SNE Research, the global power battery sales volume in 2022 will be 690GWH. There is obviously pressure to achieve a five-fold increase in the next three years.

JD Capital judged that traditional lithium has already had a phase of overcapacity and the industry is about to entert a reshuffle period.

To investigate the reasons, JD Capital believes that the rapid development in the past mainly stems from the production capacity and cost advantages brought by China’s relatively complete industrial chain, overlaid with the rapid release of domestic and foreign demand. However, in recent years, both factors have changed:

1)The production capacity of all lithium material companies in line with the rapid growth of the end battery factory, there is overcapacity.

2)European and American countries have put forward their own demands on the new energy chain. The global market is not shrinking but for Chinese companies, the growth rate may not be as fast as before.

But the market has not settled, the iteration of new technology is driving the industry inflection point again. This also means that the first ten years around the “lithium” positive and negative electrode materials, diaphragm, electrolyte formation of the industry pattern may be overturned in the future.

In addition, the development of battery material recycling and the trend of car companies building their own battery factories will also have a profound impact on the industry landscape.

For investment institutions, manufacturing investment looks firstly at market demand and growth rate, and secondly at the barriers of technology, cost, production system and sales channels of companies in business competition. In the long term, we also consider the resilience of the core team and the ability to iterate on products and technologies.

But today, the judgment of technological change is particularly important, especially the grasp of the tipping point is more demanding than a decade ago.

In the view of JD Capital, the critical point should be judged by the trend of new technology, and more importantly, the “economy” of the new technology: the product should be made, and there should be positive feedback from downstream customers’ small batch trial, and it should have the production cost performance and cost advantage.

Solid-state batteries, for example, are currently receiving a lot of market attention and are being touted as the ultimate answer to lithium batteries. Its core is a solid-state electrolyte, but it is still very early to be commercialized due to its high cost and poor cycling performance.

Another market hotspot is sodium ion battery. However, as the price of lithium carbonate has dived all the way down by more than 60% since 2023, the cost advantage of sodium batteries is no longer in the current production capacity has not yet been unfolded, coupled with the limitations of sodium batteries in energy density can not be broken in the short term, its replacement of lithium batteries in the passenger car scene is still too early.

In recent years, the popular 46-series large cylindrical battery, CTP technology and other new battery forms and assembly methods, there are already Tesla, Ningde Times, Yiwei Li-energy and other companies quickly layout, in the technology and market double up period, its commercialization process brings the main and auxiliary materials investment opportunities should be more attention by investors.

The iteration of manufacturing often stems from the replacement of old products by new products with lower cost and better performance. For power batteries, what is always pursued is the continuous improvement of product performance and decreasing cost. Which new technology can bring a better solution in cost and efficiency in the future, it has a better chance to become the variable that changes the industry pattern.

On the other hand, there are still plenty of opportunities in China today from the increased localization rate. China’s strengths remain in its continued ability to reduce costs, its ability to mass produce and its large enough market space and large enough room for cost reduction. This process, the huge market will also stimulate entrepreneurs to continuously reduce costs and improve efficiency through efforts and innovation.

The explosion of any new technology requires changes in the entire industry chain, which is a relatively slow process and an objective law that must be respected.

Essentially, new technologies, new materials, and new processes are also intermingled, with new technologies/new materials bringing new processes and new opportunities, as well as mature materials bringing new opportunities by meeting new demands.

Looking back at the history of China’s power battery development, industrial waves ebb and flow, technology iterations continue to allow domestic lithium enterprises to open the bending over. And right now, the new guard is just beginning.

About the new generation of power battery technology, more communication and discussion welcome to contact:libyd@jdcapital.com