Cell phone RF front-end chip industry research report

2020-08-13

|Industry Overview

The RF front-end chip is one of the core components of mobile intelligent terminal products. Its function is to convert the binary signal into a high-frequency wireless electromagnetic wave signal in the transmitting signal process and convert the received signal into a binary digital signal in the receiving signal process. The RF chip architecture includes two major parts, the receive channel and the transmit channel, specifically the power amplifier (PA), filter, low noise amplifier (LNA), duplexer, switch, etc.

5G will be officially launched for commercial use in 2020, and the penetration rate will increase rapidly in the next few years, making the trend of a new round of high-speed growth in the RF front-end industry clear. The global cell phone RF front-end and devices market will be around USD 16 billion in 2019 and may grow to around USD 30 billion by 2023 at a GAGR of 17%. Power amplifiers (PA) and filters as the two core chips are expected to increase in varying degrees.

|Industry Driven

RF front-end chip market threshold is high, and the industry is highly concentrated. Skyworks, Qorvo, Broadcom and Murata four vendors global market share of more than 85%. The degree of monopoly in each segment from low to high is: RF switched and antennas, PA, filters and RF front-end modules. Among them, PA is mainly monopolized by the three major manufacturers, and Broadcom and Murata primarily monopolize filters.

Domestic companies are developing from the low end to the middle and high end, and companies with solid technology accumulation have good growth opportunities. The gap between domestic RF front-end chip companies and foreign leaders is large, but after several years of expansion, they occupy a place in 2G and 3G,and begin to expand to 4G and 5G. In the field of PA, seven more mature enterprises have been formed. Namely, Heisi, Videotron, Onridge Micro, Raidec, Nationwide FeiChong, Huizhi Micro and Jusheng Micro, and two to three leading companies are expected to be formed eventually. Low-band filters have achieved mass production in the field of filters, while mid-end and high-end filters are in their infancy and have not yet created a stable competitive pattern, with both mature companies and startups having the opportunity to win.

The next three years face two key competitive elements: (1) enter the supply system of the four major domestic cell phone manufacturers to promote 4G and 5G PA import substitution; (2) achieve mass production in 5G filters to fill the domestic gap, and eventually form the RF front-end integration capability.

|Industry Risk

(1)Market competition risk: Qualcomm, Heisi, Ziguang Zhanrui, and other cell phone baseband chip companies began to extend into the field of RD front-end, and market competition intensified. Domestic companies that have not yet entered the head supporting system face the pressure of declining performance.

(2)Technology risk: the gap in filter technology between domestic companies and foreign leaders is significant, and technology breakthroughs with greater uncertainty.

Part one Industry Overview

1.1 RF Front-end Chip Industry Overview

The RF front-end chip is one of the core components of mobile intelligent terminal products. Its function is to convert the binary signal into a high-frequency wireless electromagnetic wave signal in the transmitting signal process and convert the received signal into a binary digital signal in the receiving signal process. The RF chip architecture includes two major parts, the receive channel and the transmit channel, specifically the power amplifier (PA), filter, low noise amplifier (LNA), duplexer, switch, etc.

1.2 Communication Industry Development Overview

1.2.1 Communication industry development process

Mobile communication development has gone through the process of 1G to 5G. Among them, 1G (the first-generation mobile communication system) is an analogue cellular mobile communication with poor anti-interference performance, while the simple use of FDMA technology leads to low-frequency reuse and system capacity. 2G (second-generation mobile technology) incorporates multiple access technologies, including TDMA and CDMA, while 2G is a digital communication and is, therefore, much more resistant to interference.

The main change of 3G compared to 2G is the adoption of CDMA technology, which expands the spectrum, increases the spectrum utilization, improves the rate, and is more conducive to Internet services.

4G is the application of a range of new technologies. 4G communication is faster, more flexible and more intelligent. Meanwhile, 4G requires cell phones to support multi-mode and multi-frequency, with higher requirements for baseband chips and RF front-end, forming a few cell phones chip leaders such as Qualcomm, MediaTek, Hesi, and Spreadrum.

5G technology is now opening up for mass commercialization, and 5G will feature high broadband, low latency, and broad connectivity. The transmission speed is hundreds of times faster than that of 4G networks. The core principle is to transmit signals through ultra-high frequency and rate.

In general, the development of each generation of communication technology is formed by the superposition of many minor technological upgrades. Reflected in the RF front-end chip, it is manifested in the requirement for the chip to process higher and higher frequencies and to process more and more information. It is worth noting that the development of 5G is a gradual process in which 4G and 5G will coexist and complement each other.

1.2.2 5G development trend

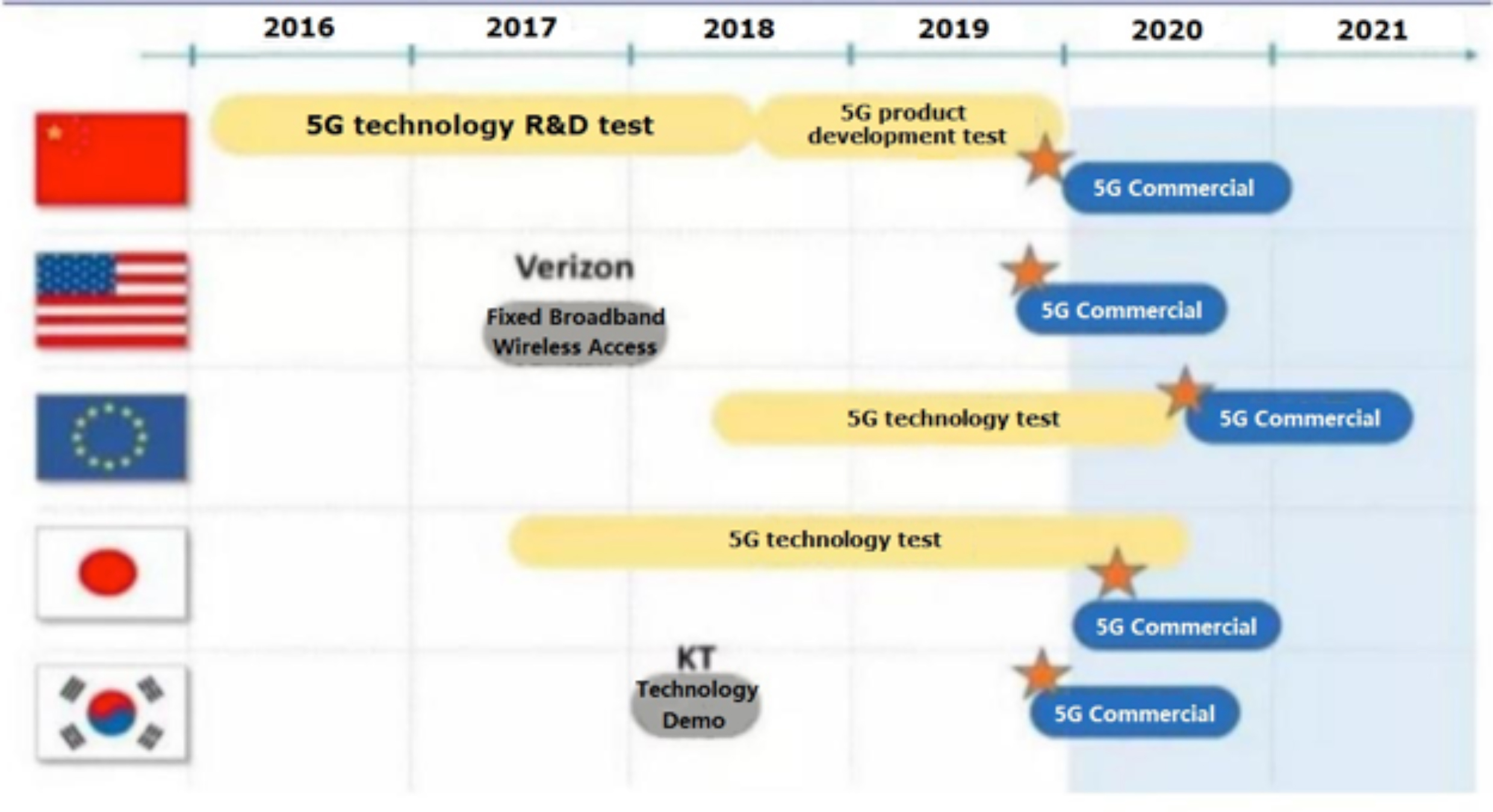

In terms of standards, in June 2019, the 3GPP (Third Generation Partnership Project) announced that the first release (version) of the 5G standard, R15, was all but complete and frozen. R16 legal development was underway and expected to be frozen in 2020. R16, the second phase standard version, focuses on vertical industry applications and overall system enhancements. According to the deployment in most countries, the global market will fully enter the 5G commercial phase in 2020.

Figure 3: Major national 5G promotion plans

Source: China ICT Academy, JD Capital

From a technical point of view, 5G RF technology is divided into two main parts: network technology and wireless technology.

Part two Industry Market Size

2.1 Cell phone market size

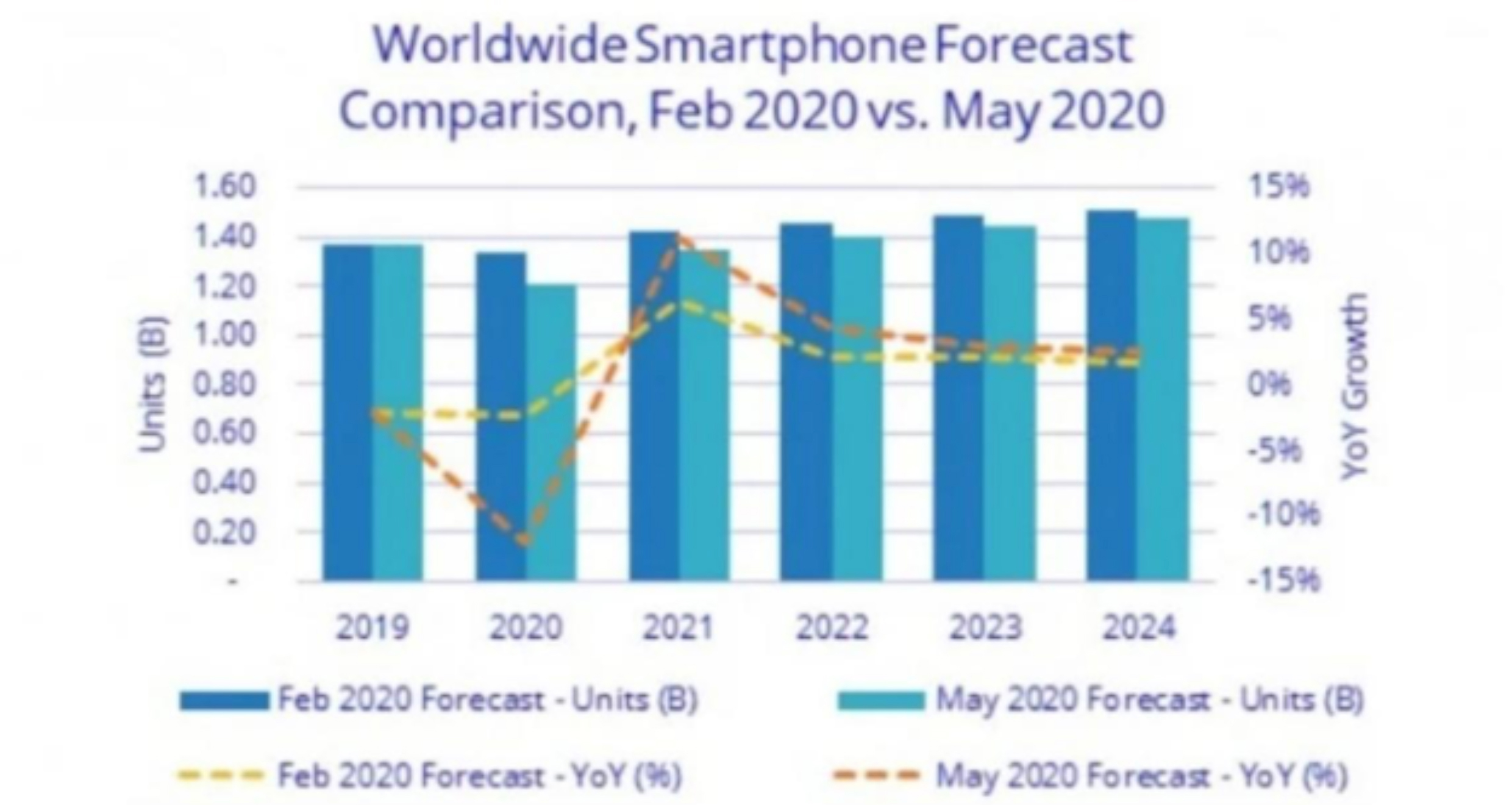

According to an IDC report, global cell phone sales in 2019 will be 1.37 billion units, and full-year 2020 cell phone sales are expected to decline another 11.9% year-over-year due to the impact of the epidemic. 5G handsets will play an important role in the recovery of the global cell phone market in 2020 and beyond. Global cell phone growth is expected to resume in the first quarter of 2021, driven by the release of 5G handsets, and to return to 1.4 billion units shipped per year in 2022.

Figure 4: IDC’s latest global smartphone shipment forecast

Source: IDC 2020 report

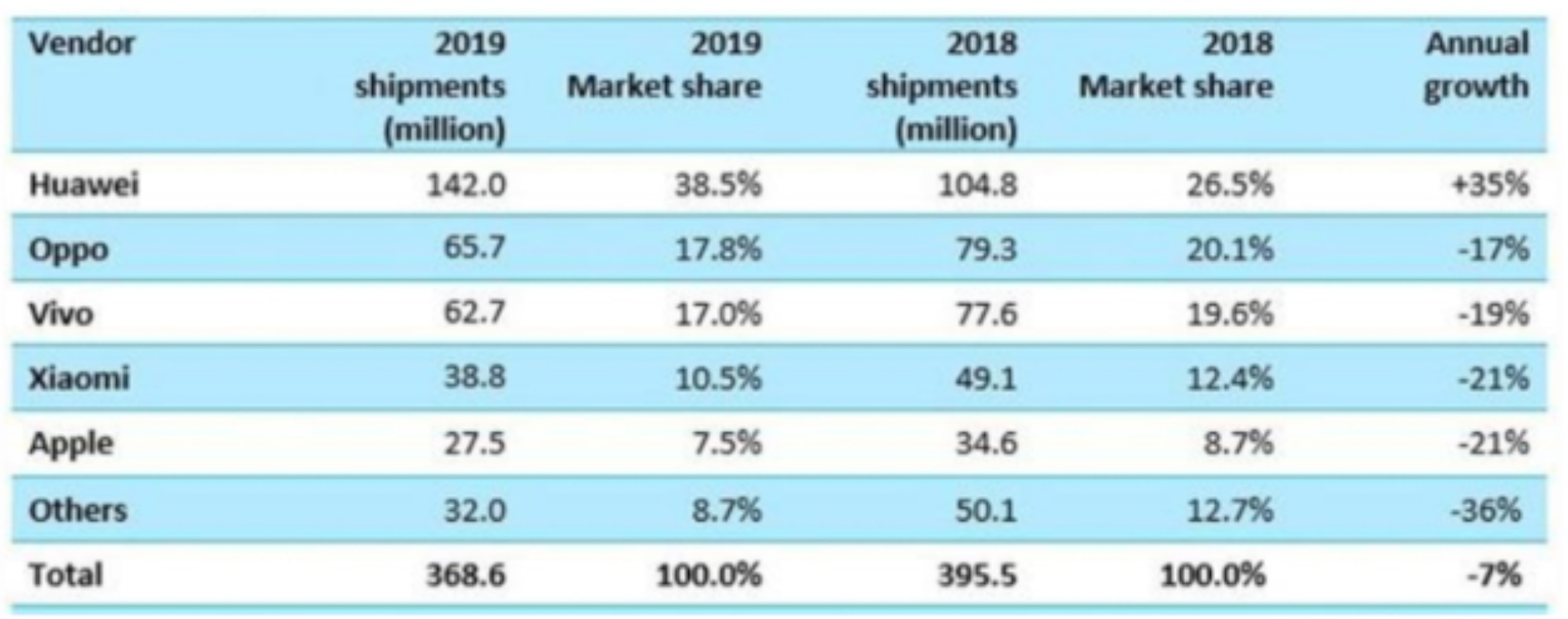

The Chinese smartphone market shipped approximately 370 million units in 2019, down 7.5% year-over-year, slowing from the year-over-year decline in 2018 (10.5%). At the same time, industry concentration increased again, with four cell phone manufactures - Huawei, OPPO, VIVO and Xiaomi - accounting for 84.4% of China’s market share, up 6 percentage points year-on-year. Among the domestic brand cell phones, the four major players (Huawei, OPPO, VIVO and Xiaomi) have achieved a market share of over 90%.

For 5G cell phone, the 5G cell phone shipments in the Chinese market will be about 9.3 million units in 2019. Huawei has an absolute advantage in China’s 5G handset market with a market share of 73.6%, followed by VIVO with a 13.7% market share. Due to faster investment in 5G infrastructure construction and higher cell phone consumption levels, China’s 5G cell phone penetration rate may reach 25% in 2022, higher than the global average. Overall, it is estimated that the average annual shipments of China’s smartphone market will be around 400 million units in the next five years.

Figure 5: Smartphone shipment in China in 2019

Source: UK research agency Canalys

2.2 RF front-end market size

2.2.1 Global market size

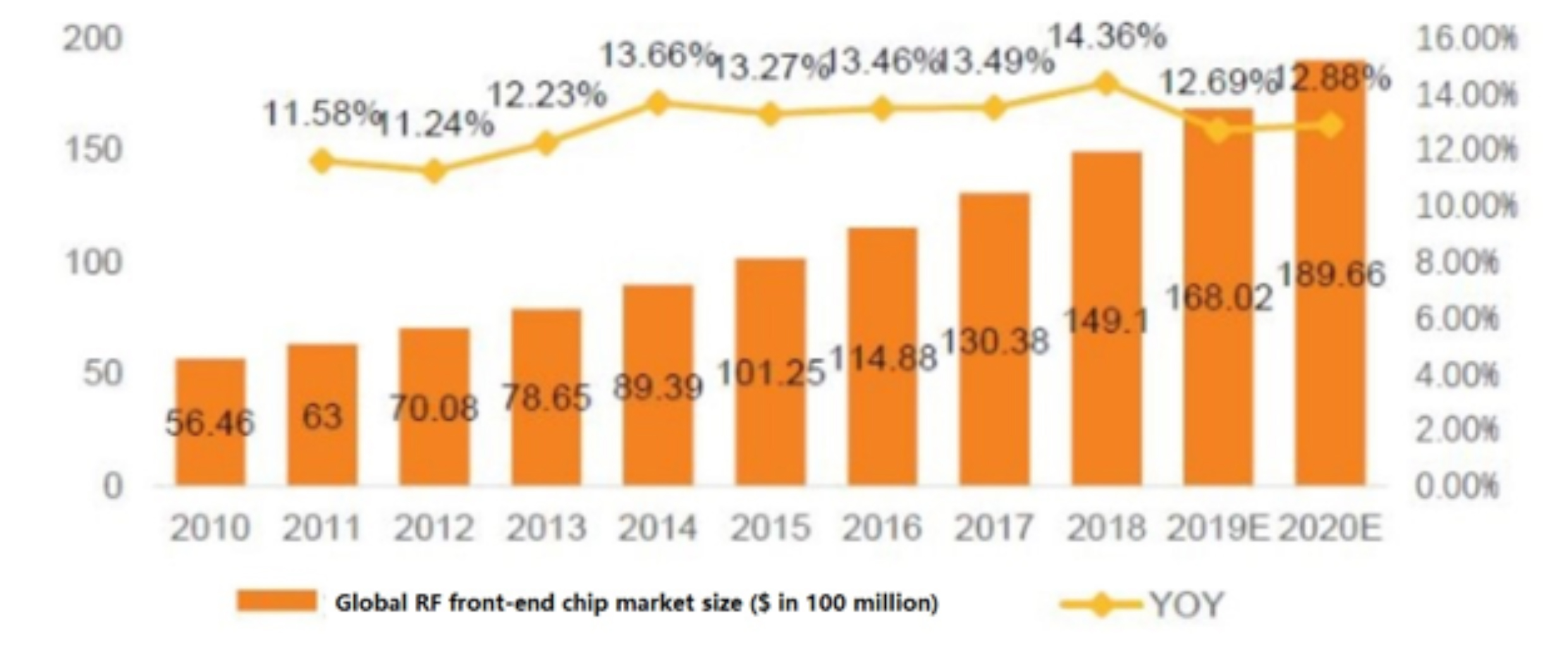

With the trend of multi-mode cell phone (communication mode increase) and the number of frequency bands increasing, the number and value of cell phone RF devices are rapidly increasing.Comprehensive global RF front-end market research reports released by a number of institutions, the global cell phone RF front-end and device market size in 2019 is about $16 billion or will grow to about $30 billion by 2023, with a compound annual growth rate of 17%, of which RF front-end modules, filters, power amplifiers (PA), low-noise amplifiers (LNA), antennas and switches will all gain varying degrees of growth.

RF front-end module is a solution that combines two or more discrete devices, such as RF switches, low-noise amplifiers, filters, duplexers, and power amplifiers, into a single module, thus improving integration and performance and miniaturizing the size.

Figure 6: Global RF Front End Market Size Trends

Source:QYR Electonics Research Center

1. PA

The number of PAs for a multimode multi-band 4G phone is about 5, while 5G phones will require 8-10 PAs, while the value volume of a single one will also increase significantly. Comprehensive Yole Development and many other authorities, the global cell phone RF PA market size is about $4.3 billion in 2019, and by 2023, the market size will reach about $6 billion. At present, 2G and 3G cell phone PAs mainly use the RF CMOS process, but in the 4G and 5G era, mainly the GaAs process is dominant, supplemented by RF CMOS.

2. Filters

Filters are the largest segment of the RF front-end market size and will grow at a high rate in the future. Comprehensive Yole Development and many other authoritative organizations' data, the global cell phone RF filter market size will grow from $9.2 billion in 2019 to $16 billion in 2023. The filter market is mainly divided into two categories, SAW and BAW.

3. LNA

While general amplifiers introduce noise while amplifying signals, RF low-noise amplifiers are widely used as they can suppress noise to the maximum extent. According to Global Radio 2019 data, the global RF low-noise amplifier revenue is about USD 1.5 billion in 2019, and the commercialization of 5G will drive the global RF low-noise amplifier market to usher in high growth in 2020, and the market size will reach USD 1.8 billion by 2023.

4.RF Switch

The RF switch is used for the selection and switching of different receiving/transmitting paths to the antenna, in order to share the antenna and save the cost of the end product. At present, RF switches mainly use the SOI process, which has the advantages of high integration and relatively low production cost, and there are many domestic foundries that can provide the SOI process. In addition, RF switches and PAs are mostly used together, so domestic PA manufacturers usually integrate the switches into modules for sale. Comprehensive Strategy Analytics and Yole Development analysis, 2019 RF switch market size of about 1.9 billion U.S. dollars, the next five years at a compound annual growth rate of more than 15%.

5. The RF module

The RF module is divided into a receiver module and a transmitter module. The receiver module consists of LNA, filter, and switch, and the transmitter module consists of PA, filter, and switch. According to Yole Development, the RF front-end receive module market is expected to grow from USD 2.6 billion in 2019 to USD 2.9 billion by 2025, at a CAGR of 2%. The transmit module market is expected to grow from $6.5 billion in 2019 to $10.4 billion by 2025, at a CAGR of 8%. As a result, the RF front-end module will grow from $9.1 billion in 2019 to $13.3 billion in 2025, at a CAGR of 6.6%.

2.2.2 China Market Size Analysis

In terms of quantity, a cell phone can support 4-7 communication modes (TD-SCDMA, WCDMA, GSM, etc.), and one communication mode contains several frequency bands. As the number of communication modes and frequency bands supported by a cell phone increases, the demand for power amplifiers (PAs), low-noise amplifiers (LNAs), duplexers, antennas, switches, and filters will also increase accordingly.

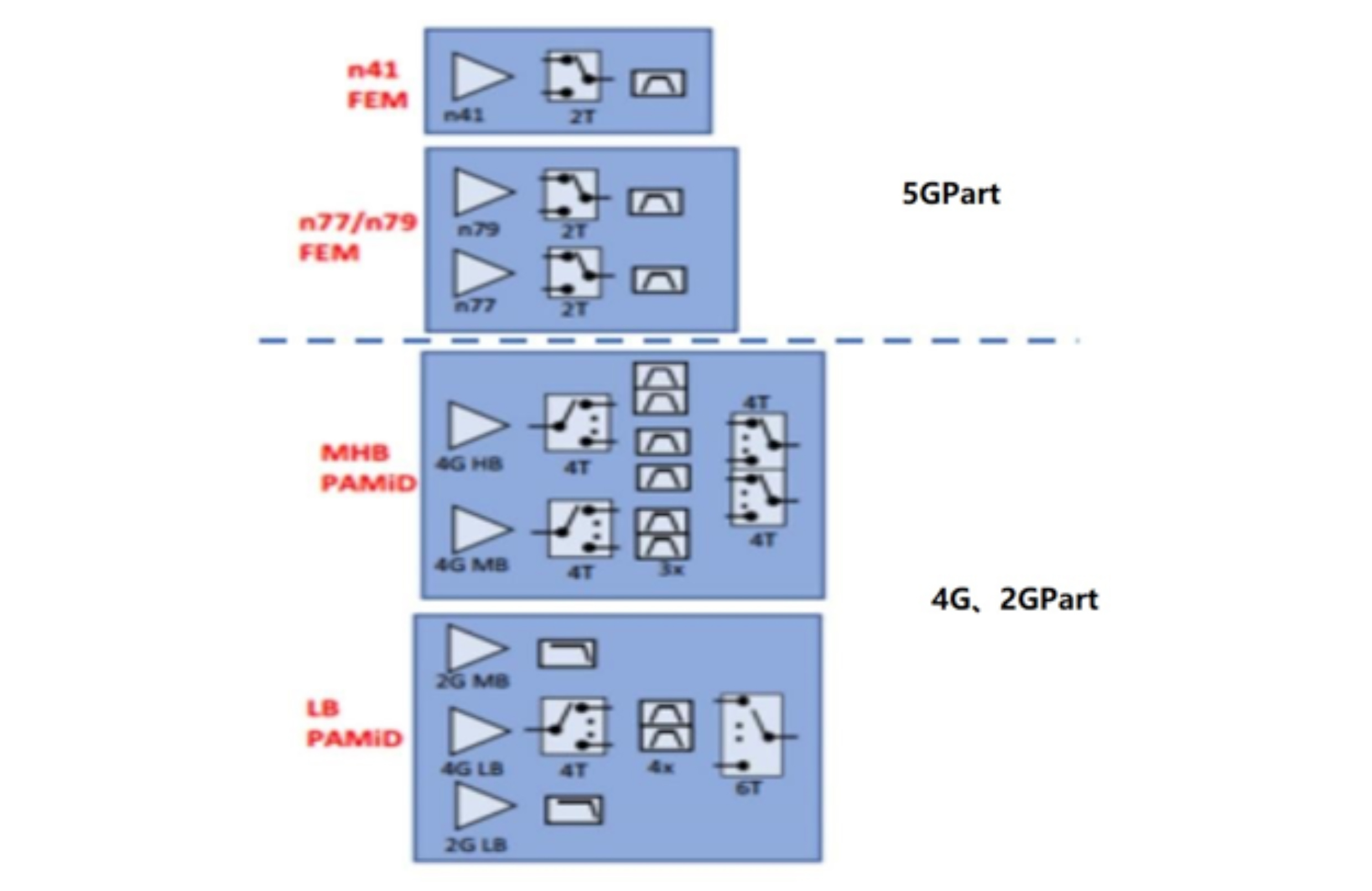

Figure 8: 5G Mobile PAMiD Solution

In terms of value volume, the growth of quantity and price changes need to be considered comprehensively. As the localization rate of the 4G cell phone RF front-end increases, the unit price of each part of the 4G RF front-end will gradually decrease, where the price of devices decreases more than that of integrated modules. For example, the current price of a 4G PA has been reduced by half compared to the beginning of 2014. However, the 5G RF front-end is still in the early stage of development and will maintain a higher price for a period of time. Therefore, the market size of the 4G cell phone RF front-end will gradually decrease, and the market size of the 5G cell phone RF front-end will grow at a high speed.

In the long term, the value volume of cell phone RF front-end has increased from 0.3 USD in the 2G era to 3.75 USD in the 3G era, then to 11 USD in the 4G era, and may reach more than 20 USD in the 5G era.

Based on the above analysis, we have estimated the RF front-end market size for domestic brand cell phones. 2019 market size is about USD 8.2 billion and will reach USD 14.06 billion by 2023. Among them, the PA market size is US$3.74 billion and the filter market size is US$6.08 billion. Although this market size is slightly smaller than Yole Development's forecast, it can still be seen that the domestic cell phone RF front-end market has a very broad import substitution prospect, and the upstream RF chip/device and module manufacturers will usher in huge development opportunities.

Part Three Competitive Analysis

3.1 Global Competition

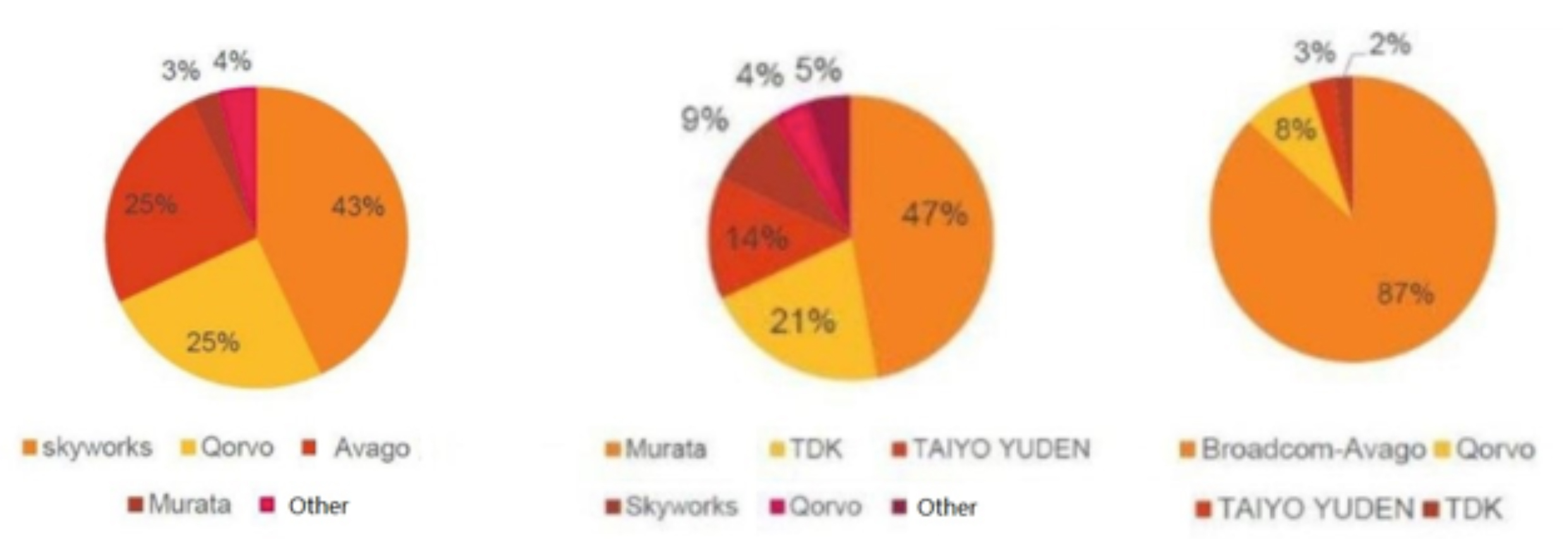

On a consolidated basis, Skyworks, Qorvo, and Broadcom are the three largest RF front-end chips/devices, accounting for about 85% of the market. By each segment, PA field: the three main chip companies Skyworks, Qorvo, the Broadcom occupy 93% of the global market share. Filter field: three Japanese companies Murata, TDK, and Taiyo Yuden occupy 82% of the global SAW filter market share, and Broadcom occupies 87% of the global BAW filter market share.

Figure 9: Global PA Competition Pattern, Global SAW Filter Competition Pattern, Global BAW Filter Competition Pattern

Source:Gartner、JD Capital

With the advent of the 5G era, industry giants such as Skyworks and Qorvo have introduced more integrated RF module solutions that benefit companies that also have the R&D and design capabilities of filters, power amplifiers, switches, etc.

1. Skyworks

Skyworks, headquartered in the United States, is a world leader in RF and infinite semiconductor solutions focused on providing a diverse range of standard and custom linear products to support automotive, broadband, energy management, industrial, medical, defense, and cell phone devices. The company is listed on the NASDAQ under the ticker symbol SWKS. in 2019, Skyworks had revenue of $3.37 billion, down 13.6% year-over-year.

2. Broadcom

AvagoTechnologies, a Broadcom company, is a supplier that designs, develops, and delivers a broad range of analog semiconductor devices to customers worldwide, with a focus on compound III-V semiconductor products. The company has superior capabilities in high-performance design and integration and a broad and diverse product portfolio with approximately 6,500 products in four key target markets: wireless communications, wired infrastructure, industrial and automotive electronics, and consumer products and computer peripherals. Avago is listed on the NASDAQ under the symbol AVGO. broadcom's 2019 revenue of 22.6 billion, up 8.4% year-over-year. Of this, the RF segment contributed revenue of $2.2 billion.

3. Qorvo

Qorvo is a provider of RF solutions formed by the merger of two companies, RFMicroDevices, and TriQuint Semiconductor, through a reciprocal merger. Qorvo's primary business is the application of RF solutions that incorporate Qorvo's creation and delivery of performance and packaging technologies to mobile devices, network infrastructure, and defense. The company's key products include amplifiers, integrated modules, control products, fiber optic components, and switches. One of its major strengths is the ability to offer both Saw and Baw. Qorvo is listed on the NASDAQ under the ticker symbol QRVO. qorvo 2019 revenue of $3.09 billion, up 4% year-over-year.

4. Murata

Founded in Kyoto in 1944, Murata is a world-leading designer and manufacturer of ceramic passive electronic components, wireless connectivity modules, and power conversion technologies. Its SAW filter market share exceeds 45% and its connection module market share exceeds 60%. 2015 acquisition of Peregrine, which specializes in RF switching and SOI technology, the two jointly launched the first fully integrated RF front-end solution. The company's fiscal 2019 (April 2019-March 2020) revenue is $14.8 billion, down 2.6% year-over-year.

5. Qualcomm

Qualcomm first entered the RF front-end field with its envelope chip and then entered the PA market with its vertical layout in the industry chain. In 2017, Qualcomm formally entered the core RF front-end field through a joint venture with TDK to establish RF360, a Qualcomm-led front-end company. Qualcomm has the strongest baseband chips and TDK has the best filters and modules, so the joint venture RF360, as the name implies, aims to create a full-coverage RF front-end platform.

As Qualcomm can provide complete RF front-end solutions, and its products cover filters, PAs, LNAs, RF switches, antenna tuning, envelope chips, front-end modules, etc. that support global networks and frequency bands, it has the necessary conditions to be a top-tier RF front-end manufacturer. With the baseband subsidy bundle plus, its front-end market share increased from 5% to 15% in the joint venture year, so it is expected to seize the leading position in the 5G RF front-end upgrade. The company's 2019 operating revenue was $24.3 billion, up 7% year-over-year. Qualcomm did not detail RF front-end revenue in the report but noted that the segment doubled from last year.

6. LODA Technology

LODA Technology is located in Taiwan and was acquired by MediaTek in 2017. The company is dedicated to developing highly integrated circuits for wireless communications, providing customers with a wide variety of RF/mixed-signal integrated circuit components and complete Bluetooth/Bluetooth low-power system single-chip solutions at high performance and low cost. The products mainly include RF switches (T/RSwitch), low noise power amplifiers (LNA), digital TV and set-top box satellite (DVB-S/S2) tuners, WiFi RF transceivers, and Bluetooth system-on-a-chip. LODA's RF products are mainly focused on the low and mid-range segments.

3.2 Domestic RF front-end chip industry status

Due to the high technical threshold of RF chips, the market has been dominated by foreign enterprises. In 2010, Taiwan and mainland China began to appear a number of new companies in the field of RF analog chips, including Hesi, Vantage Core, Aonray Micro, RuiDike, National FeiChong, Huizhi Micro, and Jusheng Micro. Domestic RF front-end chip companies account for only about 5% of the global market share, the main customers are still domestic white-label cell phones. Therefore, entering the supply system of the four major domestic cell phones is one of the key links for the development of domestic RF chip companies.

Vantage Technology is the technology leader in 4G and 5G power amplifiers, and has become the first company to enter the four major domestic cell phone brands; ONR Micro has the largest 2G market share and plans to lay out filters; Jusheng Micro focuses on RF switches and low-noise amplifiers at the low end of RF chips; Huizhi Micro and Nationwide FeiChong have shipped smaller quantities of 4G PAs, but has launched 5G PA samples.

3.2.1 Power amplifier

After several years of accumulation, domestic power amplifier manufacturers have matured in the 2G and 3G fields, and there is a trend of white-hot competition. Head manufacturers and start-up teams are beginning to expand into 4G and 5G to seek new growth opportunities.

1. Vantage Technology

Vantage Technology is a fabless IC design company founded in 2010, which started to make profits in the second year of its establishment, and the company has now entered the mature stage. Its main business is the R&D, production, and sales of RF chips. The products and services provided by the company are widely used in mobile terminals such as cell phones and tablet PCs. The company's main products include RF power amplifier chips for smart terminals, RF antenna switch modules, and RF front-end IC modules. in April 2019, a subsidiary of MediaTek made a strategic investment in VTech.

VTech's GaAs process-based chip design technology and process accumulation are leading among domestic companies. As of the first half of 2019, VTech 4G PA has entered Huawei, Xiaomi, and OPPO cell phones, becoming the only domestic power amplifier vendor to enter the four major cell phone brands and achieving explosive growth in its annual performance. Vantage Technology is expected to launch 5G PAs soon.

2. ONR Micro

ONR Micro is a leading manufacturer of wireless RF chips, smartphone amplifier chips, duplexers, and filter chips in China. 2G CMOS PA has a global market share of over 50%, ranking first in the world. By the end of 2018, the cumulative sales volume of the company's 2G/3G/4G terminal RF chips exceeded 2.7 billion units, with the highest monthly shipment of 100 million units, sold to more than 160 countries and regions, of which 4G PA is less, with a cumulative shipment of 20 million sets. The cumulative shipment of the company's chips for IoT modules exceeds 50 million units. The main products of ONEX Micro are mainly 2G and 3G, with a small number of 4G products currently shipped. 2019, Xiaomi strategically invested in ONR Micro.

3. Raidec

Raidec was established in 2004. 2018, ZTE and Raidec completed the integration. Raidec is mainly engaged in the design, development, manufacture, sales, and provision of related technical consultation and technical services of RF ICs. The company's main products are divided into three categories: cell phone communication support chips, including power amplifiers, converters, and receivers; Broadcast communication chips, including FM, set-top box RF reception, mobile TV signal receivers and tuners, satellite TV HF heads; wireless data connection chips, including Bluetooth, Bluetooth, and FM 2-in-1, Wi-Fi, Bluetooth and FM 3-in-1, wireless walkie-talkies. The company has many cell phone customers at home and abroad including ZTE, Huawei, TCL, Tianyu, Samsung, etc.

4. National FeiChong

In 2010, the National FeiChong team started to develop domestic RF power amplifiers and RF switches relying on the domestic market. 2015, National FeiChong was separated from National Technology. 2011, its NZ5081 was applied to Yulong Coolpad 8180 TD-SCDMA cell phone, which was the first domestic PA applied to smartphones (RDA was the first PA applied to domestic feature phones). Since 2015, the National FeiChong has entered the supply system of Redmi, Coolpad, ZTE, Meizu, etc. In 2020, FeiChong released its self-developed 5G front-end solutions, including the LPAMIF module of N77+N79, etc.

5. WiseChip

Founded in November 2011 and started operations in early 2012, WiseChip is the world's first chip company to reconfigure multi-band, multi-mode RF front-end technology, and mass produce it. WiseChip's innovative reconfigurable hybrid integrated RF front-end architecture technology can be applied to RF power amplifiers and other RF front-end devices for 4G mobile terminals. Currently, WiseChip's revenue volume is small. 2019 saw the launch of a 5G reconfigurable RF front-end platform and self-research power amplifiers.

6. Zhongpu Microelectronics

Zhongpu Microelectronics is engaged in RF IC design, R&D, and sales, with products covering GSM, W-CDMA, TD-SCDMA, CDMA2000, and the rapidly evolving TD-LTE, providing comprehensive RF front-end solutions for 2G/3G/4G. In 2014, the listed company Weir Corporation took a controlling stake in Zhongpu Microelectronics. Currently, there are no RF devices for 5G in Zhongpu Microelectronics.

7. Other

Influenced by China's accelerated 5G construction process, as well as the dual drive of trade friction between China and the United States. At present, there are also multiple forces in the research and development of RF PA. One is Huawei Heisi, which has RF R&D teams at the base station end and cell phone end, and now has the batch self-supply capability of some 4G cell phone PAs. The second is the returnee or local startup team, including the core park, hunting core, Ruishi Chuangxin, Yizhi, etc. The advantage is that it comes from a global leader with advanced design experience, the disadvantage is that the customer base is weak, especially the four major cell phone brand customers, and it takes a long verification cycle to enter its supply chain, which requires high product stability and follow-up service quality, which is a challenge for startups.

3.2.2 Filters

Domestic companies involved in filters are relatively few, mainly small batch production in research institutes, while there are companies such as Tianjin North, Wuxi Hoda, etc. mass production of SAW filters for wireless communications; listed companies such as Magitech and Xinwei Telecom launched filter products through joint research and development. In addition, there are a number of start-up Fabless companies that are developing or mass-production of filters.

In general, the domestic filter design and manufacturing level is in the initial stage, gradually beginning to launch 5G N41, and the following bands of filter products, are expected in the next 2-3 years, will successively mass production of N77/78, N79 and other major bands of 5G filter products. At present, domestic startup filter companies are in the form of Fabless, and some of them are planning to build filter production lines.

1. MJ Technology

The company issued an additional $850 million in 2016, of which $372 million was used for the development and production project of a terminal RF acoustic surface filter (SAW) packaging process based on LTCC substrate. It signed a strategic cooperation agreement with Chongqing Acoustic Optoelectronics Group in May 2017, in which both parties cooperate in the micro-acoustic filter (SAW, TC-SAW, FBAR, etc.) products and set up a joint venture company, in which MJT holds 35% equity.

2. Xinwei Communications

The company signed a strategic cooperation agreement with China Electronics Technology Group 55 in June 2017, and Xinwei Communication holds the equity of Deqing Huaying by increasing the capital of Deqing Huaying by 110 million yuan, and the two sides will cooperate in the convenience of sound surface filters, 5G high-frequency devices and GaN power devices; the domestic listed company of sound surface filters and the research institutes in the United Nations, combining the capital advantage of the listed company with the listed company of domestic sound surface filter and the research institute will combine the capital advantage of the listed company and the technical strength of the research institute to accelerate the large-scale industrialization of the filter.

3. Norse

Founded in 2011, headquartered in Tianjin, with total registered capital of RMB 300 million, the company is the first FBAR manufacturer in China, which is engaged in the design, development, manufacturing, and sales of RF front-end MEMS filter chips, modules, and application solutions for wireless devices, with core products reaching international leading level. In 2018, the capacity of the Tianjin NOS factory is 30 million WIFI filters. The company plans to invest in a new filter production line in Mianyang.

4. Wuxi Hoda

The company was founded in 1999 and is a company with many years of experience in filter production, but the products are mainly used in microphones, navigation, and other low-end areas, there are no filter products for cell phones. In early 2020, Huawei's strategic investment in good, its BAW filter is expected to gradually enter the cell phone field.

3.2.3 RF Switch

In the field of RF switches, the entry threshold is relatively small compared to a power amplifier and filter. With its mature process, Jusheng Micro has become the largest RF switch company in China. Founded in 2012, JOSUN Micro's main business is RF switches and RF low-noise amplifiers. Due to its excellent RF CMOS process, it has successfully entered the supply chain of well-known customers such as Samsung and Huawei. Jusheng Micro achieved revenue of 1.5 billion RMB and a net profit of 497 million RMB attributable to the mother company in 2019. After the successful listing of Jusheng Micro, the funds raised further enriched the product line structure, laying out filters, high-performance antennas, RF front-end modules, low-power Bluetooth, and other products. At present, the company has shipped a number of SAW filters in mass production and started to invest in the research and development of BAW filters.

In addition to Jusheng Micro, the above-mentioned major PA manufacturers, and some filter manufacturers have also started to launch their own design and development of RF switches, and the market competition in this field has intensified.

Part four Summary

With the arrival of 5G and the era of the Internet of everything, the number of RF has increased significantly, and RF front-end chips will usher in a new round of high-speed growth period. In the global scope category, foreign leaders still hold the main technology and the vast majority of the market. Domestic companies started from the low-end, and now have entered the mid-to-high-end market in the field of switching and low-noise amplifiers; in the field of power amplifiers with a larger market size, the country is in the stage of about to enter the mainstream domestic cell phones; in the field of filters with the largest market size, domestic manufacturers are actively laying out. Specifically:

1. 5G in 2020 to officially open commercial, the next few years penetration rates will rapidly increase, RF front-end industry a new round of high-speed growth trend is clear. 2019 global cell phone RF front-end and device market size of about 16 billion U.S. dollars, to 2023 or will grow to about 30 billion U.S. dollars, a compound annual growth rate of 17%. The power amplifier (PA) and filter as the two core chips will usher in different degrees of rapid growth.

2. RF front-end chip market threshold is high, and the industry is highly concentrated. four major vendors Skyworks, Qorvo, Broadcom, and Murata global market share of more than 85%, the degree of monopoly in each segment from low to high are RF switch and antenna, PA, filter, and RF front-end module. Among them, PA is mainly monopolized by the three major manufacturers, and the filter is mainly monopolized by Broadcom and Murata.

Domestic companies are developing from low-end to mid- to high-end, and companies with solid technology accumulation have good growth opportunities. The gap between domestic RF front-end chip companies and foreign leaders is large, but after several years of accumulation, they occupy a place in 2G and 3G and start to expand to 4G and 5G. In the field of PA, there are 7 more mature companies, including Heisi, Vantage Core, Angry Micro, Raidec, Nationwide FeiChong, Huizhi Micro, and Jusheng Micro, and it is expected that 2-3 leading companies will be formed eventually; in the field of filters, low-band filters are in mass production, mid and high-end filters are in the initial stage, and a stable competition pattern has not yet been formed, so both mature companies and startups have opportunities to win.

We believe that the next three years is a critical period for the development of domestic RF front-end chip companies: first, excellent RF companies will gradually enter the supply system of the four major domestic cell phone manufacturers to promote the import substitution of 4G/5G PAs and filters; second, the 5G market, which will open in 2019, will last at least five years, and companies that achieve technological catch-up in some segments will share the 5G dividend to achieve high growth.